Yawn. One jackass sells, another one moves in. The trees gotta shake once in a while. I can't believe you live less than 7 miles from me and you've never wanted to discuss this in person, over beers. Move back over there, you jackass. Just let me know before you leave ok?Originally Posted by Benny Profane

Results 776 to 800 of 28452

Thread: Real Estate Crash thread

-

05-29-2008, 12:50 AM #776

skier

skier

- Join Date

- Dec 2002

- Location

- The Garden State

- Posts

- 4,895

-

06-01-2008, 11:53 AM #777

Registered Abuser

Registered Abuser

- Join Date

- Mar 2005

- Location

- Yonder

- Posts

- 22,528

In some areas of California, so many foreclosed homes are available to buy on the cheap that real estate agents are discouraging prospective sellers from even putting their houses on the market.

Perhaps the most extreme example of this is Stockton, about 85 miles east of San Francisco, where roughly three of every four homes for sale are in or on the path to foreclosure.

The city's resale market is "pretty much gone," said Cameron Pannabecker, owner of Cal-Pro Mortgage.

"I don't know an agent today who would take your listing unless you're a hard-luck case. There is just too much competition," Pannabecker said.

Properties that at the peak of the market two years ago were selling at $500,000, or appraised at $500,000, are now selling for $200,000, he said.

http://www.cnbc.com/id/24886877Kill all the telemarkers

But they’ll put us in jail if we kill all the telemarkers

Telemarketers! Kill the telemarketers!

Oh we can do that. We don’t even need a reason

-

06-01-2008, 01:57 PM #778

Registered User

Registered User

- Join Date

- Mar 2006

- Posts

- 20,162

Houses in my entry level Bay Area California neighborhood are selling. Dump two houses down just sold for around $300k. It's a hideous house.. Prices in my neighborhood are in line with incomes and compete directly with renting now.

-

06-01-2008, 03:11 PM #779

Banned

Banned

- Join Date

- Oct 2003

- Location

- Looking down

- Posts

- 50,490

http://www.economist.com/world/na/di...ry_id=11453745

"The S&P/Case-Shiller national index fell by 14.1% in the year to the first quarter. Admittedly, other property indices show smaller drops, but most economists now favour this measure. The index goes back only 20 years, but Robert Shiller, an economist at Yale University and co-inventor of the index, has compiled a version that stretches back more than a century. This shows that the latest fall in nominal prices is already much bigger than the 10.5% drop in 1932, at the worst point of the Depression."

And the Wall Street Journal has a guy snooping around down in the Florida real estate market coming up with some fascinating observations, if numbers bore you. Check it out. He called some homes down there "valueless", because they were built inland around phantom golf courses, and are now sitting empty without much hope.Last edited by Benny Profane; 06-01-2008 at 03:15 PM.

-

06-01-2008, 04:20 PM #780

semi pro hedonist

semi pro hedonist

- Join Date

- Apr 2005

- Location

- The land of Genesee Cream Ale and homemade pierogies!

- Posts

- 2,158

I read those articles the other day. Interesting reading to put it mildly. A quote "The market is in chaos. Some owners are still trying to sell homes for near peak prices. Others have slashed them by 50% or more. There are some amazing discounts around. You can find properties selling for prices last seen in the late 1990s." Originally Posted by Benny Profane

Read at no cost:

The Truth Behind Florida's Housing Numbers

You Don't Have to Be Rich to Own a Home on the Beach

There's also a video to go with those write ups: http://link.brightcove.com/services/...ctid1579816481

-

06-05-2008, 09:58 AM #781

Registered User

- Join Date

- Apr 2006

- Posts

- 308

It's not just a US problem...UK is bleeding:

http://www.newstatesman.com/economy/...ousing-british

-

06-05-2008, 02:38 PM #782

...darkness is beautiful

...darkness is beautiful

- Join Date

- Nov 2003

- Location

- P-tex, CA

- Posts

- 8,748

-

06-05-2008, 02:43 PM #783

Registered Abuser

- Join Date

- Mar 2005

- Location

- Yonder

- Posts

- 22,528

Kill all the telemarkers

Kill all the telemarkers

But they’ll put us in jail if we kill all the telemarkers

Telemarketers! Kill the telemarketers!

Oh we can do that. We don’t even need a reason

-

06-05-2008, 02:59 PM #784

ExteriorDecorator

ExteriorDecorator

- Join Date

- Nov 2005

- Location

- Down In A Hole, Up in the Sky

- Posts

- 36,476

Forum Cross Pollinator, gratuitously strident

Forum Cross Pollinator, gratuitously strident

-

06-05-2008, 05:45 PM #785

Registered Defector

Registered Defector

- Join Date

- Mar 2005

- Location

- The Alps

- Posts

- 2,639

So, would it be safe to say the shit has hit the fan?

-

06-05-2008, 08:01 PM #786

Last Survivor of the NPG

Last Survivor of the NPG

- Join Date

- Aug 2007

- Location

- At the beach

- Posts

- 20,714

Well, maybe. Like the old saying goes "Location, Location, Location. Originally Posted by enlosandes

The nice beach areas in San Diego are holding even to small amounts of appreciation. Out lying areas and condos are getting drilled in San Diego on the whole.

Same thing in Orange County. Nice beach areas have little depreciation to some appreciation. That is saying something while other areas are down 30% from 2006.

I have been following resales in Mammoth (ski area). Most serious listings are at a 2004 price level and not selling. Listings are on the market forever. I think another 10% hit is there, so we will see 2003 price levels there in the next year.Never in U.S. history has the public chosen leadership this malevolent. The moral clarity of their decision is crystalline, particularly knowing how Trump will regard his slim margin as a “mandate” to do his worst. We’ve learned something about America that we didn’t know, or perhaps didn’t believe, and it’ll forever color our individual judgments of who and what we are.

-

06-05-2008, 08:10 PM #787

ExteriorDecorator

- Join Date

- Nov 2005

- Location

- Down In A Hole, Up in the Sky

- Posts

- 36,476

Same here...Downtown/east Jackson, Teton Village, Ski Hill road/Alta, holding steady, with an uptick for commercial...but land in the flats of drictonia, flat, at best, (and a 10%-15% downturn for less interesting stuff). A lot of people who bought cheap 3-10 years ago are holding their prices, but folks who bought/built in the last two years are hurting.

Anything under $300K is holding fast, that is basically bottom dollar for a private residence. (outside of a Condo Studio near the storage units)Forum Cross Pollinator, gratuitously strident

-

06-05-2008, 09:01 PM #788

Registered Defector

- Join Date

- Mar 2005

- Location

- The Alps

- Posts

- 2,639

Tahoe prices are closing in on 2002/2003 prices at the moment.

-

06-05-2008, 09:07 PM #789

Future ski-bum lifty

Future ski-bum lifty

- Join Date

- Dec 2006

- Location

- A beer fortress in the kingdom of cheese...

- Posts

- 3,742

More good news from the "Bush economy"...

Nearly 1 in 10 Homeowners Face Loan Problems

Originally Posted by NYTimes.com

If some of the best times of my life were skiing the UP in -40 wind chill with nothing but jeans, cotton long johns and a wine flask to keep warm while sleeping in the back of my dad's van... does that make me old school?

If some of the best times of my life were skiing the UP in -40 wind chill with nothing but jeans, cotton long johns and a wine flask to keep warm while sleeping in the back of my dad's van... does that make me old school?

"REHAB SAVAGE, REHAB!!!"

-

06-06-2008, 08:57 AM #790

Sniffing Polypro

Sniffing Polypro

- Join Date

- Apr 2008

- Location

- Land Of Passive Aggro

- Posts

- 322

I can smell it

I can smell it

-

06-06-2008, 11:26 AM #791

Registered User

- Join Date

- Oct 2003

- Location

- Denver

- Posts

- 1,633

of the 1 in 11 american mortgages do we have an idea how many of those are primary residences vs vacation homes, flips etc etc? Originally Posted by timvwcom

-

06-06-2008, 11:34 AM #792

Registered User

Registered User

- Join Date

- Sep 2006

- Posts

- 8,686

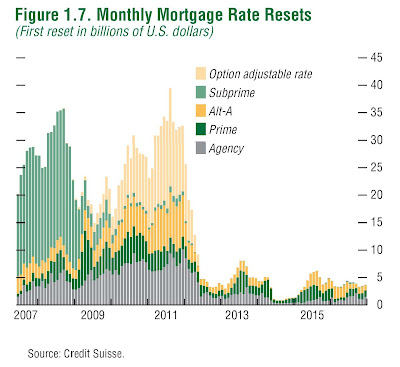

Originally Posted by Purveyor of Slack

Based on the above graph, it looks like the second shit show will start in 2010. Gee, do you think Bernake will keep Fed funds rate at 2-2.25% for another 2 years? Look for some serious democratic push for a home foreclosure bail out bill in early on '09."We don't beat the reaper by living longer, we beat the reaper by living well and living fully." - Randy Pausch

-

06-06-2008, 12:00 PM #793

Sniffing Polypro

- Join Date

- Apr 2008

- Location

- Land Of Passive Aggro

- Posts

- 322

True dat, it's the lull in the storm. Originally Posted by Toadman

BTW, MBIA and Ambac finally got their ratings cut. My guess is the Fed will cut again and probably sooner rather than later.

Conterparty risk is THE issue with all those hundreds of billions in CDS backed assets. Those AAA ratings are becoming even more meaningless...if that is possible.I can smell it

-

06-11-2008, 06:53 PM #794

Banned

- Join Date

- Oct 2003

- Location

- Looking down

- Posts

- 50,490

http://online.wsj.com/article/SB1213...alEstateMain_1

In markets hit hardest by falling home prices and rising foreclosures, lenders and brokers are discovering a new phenomenon: the "buy and bail," in which borrowers with good credit buy a new home -- often at a much lower price -- then bail out of the "upside down" mortgage on their first home.

Homeowners are able to pull off this gambit -- which some lenders and real-estate agents call mortgage fraud -- by taking advantage of mortgage-lending practices that allow them to buy a new primary residence before their existing residence has been sold. And with the lending industry in disarray as it tries to restructure millions of mortgages, some boast they are able to pull off the strategy with ease.

-

06-11-2008, 11:36 PM #795

Last Survivor of the NPG

- Join Date

- Aug 2007

- Location

- At the beach

- Posts

- 20,714

Some lenders in CA will not make you a new loan if your underwater on a present primary residence. I guess I can see why based on the above explanation, but I am not sure that is right either. Guess I will have to think about that one. Originally Posted by Benny Profane

I have been in the mortgage industry since 1984. IMO the current mortgage crisis in San Diego is no worse than when the defense industry when bust in the early 90's thanks to the policies of Bill Clinton.

What I find very puzzling this time around is how far the pendulum has swung from easy 100% financing with stated income/assets loans a year ago to now where companies will not make a fully documented loan over 60% LTV. The lenders with their incredible pullback in underwriting guidelines are creating, in many cases, a self fulfilled prophesy of declining values and consequential foreclosures due to their myopic lending practices. It is fucking mind boggling.

The lenders deserve all the foreclosures they are getting. There is never a happy medium, it is either give the money away or no money for anyone. Fuck them IMO. No bail outs for the banks.Last edited by liv2ski; 06-11-2008 at 11:47 PM.

Never in U.S. history has the public chosen leadership this malevolent. The moral clarity of their decision is crystalline, particularly knowing how Trump will regard his slim margin as a “mandate” to do his worst. We’ve learned something about America that we didn’t know, or perhaps didn’t believe, and it’ll forever color our individual judgments of who and what we are.

-

06-12-2008, 06:35 AM #796

Buy the Bros or else!

Buy the Bros or else!

- Join Date

- Oct 2003

- Location

- Wish I knew?

- Posts

- 2,752

^^Just because it is written in a newspaper doesn't necessarily mean it is true!

The pacifists always lose, because the anti-pacifists kill them.

-

06-12-2008, 10:28 AM #797

Registered User

- Join Date

- Sep 2006

- Posts

- 8,686

This may or may not be true, so take it with a grain of salt... Originally Posted by AKPogue

Many more foreclosures ahead

Foreclosures hit a record high in the first quarter, when homeowners walked away from about 448,000 mortgage loans. Matters are only going to get much worse, predicts Mark Zandi, the chief economist at Moody's Economy.com.

He bases his gloomy outlook in part on insights about worsening consumer credit trends that he gets from data compiled by Equifax, one of the credit reporting bureaus. "Foreclosures have been rising for just over two years, and they will rise for another year," Zandi says. "It is a serious problem that is not going away fast."

Zandi thinks defaults on first mortgages will jump 60% this year to 2.3 million, compared with 1.4 million last year. Then, in 2009, he expects defaults to hit 1.7 million, still 18% above last year's level. And defaults will remain at high levels "well into next decade," he says, as a delayed effect from adjustable-rate mortgages, or ARMs, kicks in.

Monthly payments on many ARMs aren't going up too much right now because they are linked to market interest rates, which are low. But the Federal Reserve will raise rates at some point, and that will create issues for borrowers in two or three years.

Meanwhile, the unrelenting decline in home values won't let up. Zandi predicts home prices will fall 12% this year and nearly 8% in 2009. This will lead to more foreclosures because it leaves a lot of new homeowners owing more than their homes are worth. This makes it tempting for them to walk away from mortgage payments when they are hit with an unexpected expense or job loss, fairly common problems because so many new homeowners have moderate incomes.

"These households are living on the financial edge, and it doesn't take much to push them over," Zandi says.

"We don't beat the reaper by living longer, we beat the reaper by living well and living fully." - Randy Pausch

-

06-12-2008, 02:29 PM #798

Last Survivor of the NPG

- Join Date

- Aug 2007

- Location

- At the beach

- Posts

- 20,714

^^^^ unless lenders really start lending again, with no declining value limitations to at least 90-95%, the foreclosures will keep a coming as ARMs reset over the next 2 years. I am sure prices will continue to decline. Out lying areas and vacation homes often get rocked the hardest, so keep your eyes open for some good deals on ski property in 2009.

Never in U.S. history has the public chosen leadership this malevolent. The moral clarity of their decision is crystalline, particularly knowing how Trump will regard his slim margin as a “mandate” to do his worst. We’ve learned something about America that we didn’t know, or perhaps didn’t believe, and it’ll forever color our individual judgments of who and what we are.

-

06-14-2008, 04:46 PM #799

Registered Abuser

- Join Date

- Mar 2005

- Location

- Yonder

- Posts

- 22,528

http://promo.realestate.yahoo.com/pr...get-worse.html

Hard hit cities like Sacramento, Phoenix and Las Vegas are set for more steep losses. Some real estate experts are bracing for price drops of as much as 50%.

NEW YORK (CNNMoney.com) -- With home prices plunging by more than 30% in some markets, bargain-hunters are ready to pounce.

But it may pay for buyers to wait. Many housing experts say that the worst-hit metro areas have even farther to fall, and could see total drops of as much as 50%.

"The housing boom was unprecedented in U.S. history," said Michael Youngblood, a portfolio analyst with FBR Investment Management, "and the correction will be as well."

High-end housing crunch, 90210

Many erstwhile bubble cities have sustained particularly brutal hits. The median- price of a home in Sacramento, Calif. was down 35% during the three months ended May 31 compared to the same period last year, according to the real estate web site Trulia.com. In Riverside, Calif. prices fell 29%, while San Diego prices dropped 26%.

Smaller cities in California's Central Valley, such as Stockton (-39%), Modesto (-37%) and Bakersfield (-29%), also recorded steep declines.

Outside California, hard-hit markets include Phoenix (-18.8%), Las Vegas (-22%), West Palm Beach, Fla. (-32%) and Cape Coral, Fla. (-35%).

Youngblood expects that these markets will likely endure total price drops of 50% or more.

The smart money

Indeed, prices are falling faster and further than in any other post-war housing bust. During the bust in Austin, Tex., which started in 1986 and is one of the worst on record, prices fell 25%, according to Local Market Monitor, a financial data provider. And that cycle took four years to bottom out.

In other major downturns, prices in Los Angeles fell by 21% during a six-year period in the 1990s, and Honolulu home prices saw a decline of 16% in the five years starting in 1994.

Youngblood's forecast "is quite plausible," said Nicholas Perna, of the economic consulting firm Perna Associates. He finds it especially significant that the smart money, investors in the S&P Case/Shiller Home Price Index, are still buying futures as if they expect prices to continue to plummet.

The index, which tracks the sale price of specific homes as they are sold and resold over the years, is considered to be one of the most accurate home price indicators.

"The people who are putting their money where their mouths are," said Perna, "are betting on more losses."

Specifically, Case/Shiller investors are betting that Las Vegas prices will fall an additional 22% by November 2009. Los Angeles futures predict a further loss of 24.2% through November 2009, while investors expect to see Miami down another 21.6% by then.

These markets may have a hard time recovering because, according to Perna, people are afraid to buy right now, because they're concerned about over-paying. That helps explain why price depreciation seems to be accelerating.

"The most severe declines are happening right now," said Mark Zandi, chief economist for Moody's Economy.com.

Prices vs. wages

This correction was inevitable, in Youngblood's opinion; home price gains had simply out-paced income by far too much to be sustained.

Historically, home prices have averaged about four times wages. Whenever homes got significantly more expensive, people could not afford to buy and home prices fell back.

But local price-to-income ratios are still out of whack even after steep price declines, which means prices have further to fall. In Los Angeles, where the ratio peaked at 22.7, according to Youngblood, it's still in the high teens. Home prices would have to come down another 40% or so to get that ratio back into the single digits.

And it's not just the housing fundamentals that lead Youngblood to expect more drops; he also cites the local economic conditions.

"Bubble cities are now seeing fleeing employment conditions," he said. In Miami, the unemployment rate rose 34.3% between April 2007 and April 2008, according to Youngblood. And the job picture in California cities, where many jobs were housing related, has been even more disastrous.

Housing was a key economic engine for towns like Riverside, Stockton and Modesto during the boom, according to Zandi. Builders, real estate salespeople, mortgage brokers and lenders, and even retailers, like Home Depot (HD, Fortune 500) and Lowe's (LOW, Fortune 500), depended on growth in the sector.

"In all those deteriorating housing markets, it's a double hit," he said.

Ten of the 11 cities with the highest unemployment rates in the nation are now in central California, with El Centro , at 18.4% in April, leading the way. Other double-digit disaster areas were in Merced (12.3%), Yuba City (11.8%), Modesto (10.7%), Visalia (10.3%), Hanford (10.2%) and Fresno (10%).

Many of these cities are also among the leaders in foreclosure rates. As more foreclosed properties hit the market, prices are further depressed.

"[The price drops] reflect a wave of distressed sales of [bank-owned] properties and discouraged sellers," said Zandi

The brighter side

Not all analysts are pessimistic. Richard DeKaser, chief economist for National City Corp (NCC, Fortune 500) points out that, thanks to the price declines, the national market is the most affordable it's been in years.

With the national median price of a single family home at $204,229, mortgage rates around 6% and the average household earning nearly $50,000, the average home buyer spent about 23.2% of their income on housing during the first quarter of 2008. That's down from 2006, when homeowners spent an average of 29% of their income on housing.

Nariman Behravesh, an economist with Global Insight, says that while he expects home prices to stagnate for the next five years, Youngblood's 50% price decline forecast is "a little extreme."

But that target is realistic, Behravesh says, after taking inflation into account. In markets where prices have fallen 35% or more, and remain depressed through five years of 4% inflation, home prices in real dollars will absorb an additional 20%-plus hit. That would push price declines to over 50%.

Of course, there are plenty of wild cards that could affect home price trends, such as the election, Congressional legislation, unemployment, gas prices, and interest rates.

"This whole market is fraught with all sorts of implications," said Perna, "and it ain't over until it's over."Kill all the telemarkers

But they’ll put us in jail if we kill all the telemarkers

Telemarketers! Kill the telemarketers!

Oh we can do that. We don’t even need a reason

-

06-15-2008, 12:46 PM #800

Don't call it a comeback

Don't call it a comeback

- Join Date

- Feb 2003

- Posts

- 6,110

It's all about cash flow.

In the long term, it can't cost more to buy a place on a fixed-rate mortgage than you can get back in rent. Further price increases are speculative.

This doesn't mean people didn't make a lot of money speculating -- just that it can't hold in the long term, because profit depends on flipping to a greater fool.

1970s, here we come again. Remember "white flight" to the suburbs? Entire neighborhoods are going to be abandoned as looters and squatters destroy unoccupied houses. But now it's almost the opposite: old suburbs are the slums now (e.g. Compton), and this will continue...but with $5 gas and foreclosures, the hardest-hit exurbs will become new slums. The rich and remaining middle class will consolidate in certain neighborhoods, primarily "urban renewal" zones for the middle class (to save commute costs), exclusive gated communities for the rich who can still afford to drive everywhere, and a few other places that are both on the water/in mountains and close to work (e.g. Hollywood hills).

Reply With Quote

Reply With Quote

Bookmarks